10 Buffettisms That Will Transform Your Investing Philosophy

Warren Buffett’s Timeless Wisdom for a successful investment strategy

Warren Buffett has beaten the market for over 65 years. He achieved a 31.6% annual return while running the Buffett Partnership between 1957 to 1968. And he’s achieved an annual return of 19.8% from 1965 to 2023 as the Chairman of Berkshire Hathaway Inc. (compared to the S&P 500 return of ~10%).

How did Warren Buffett compound his wealth at such astronomical rates for such a long period of time? What principles, philosophies did he use to achieve it?

Let’s unpack the 10 investing principles that Buffett used to achieve phenomenal success in his investing career:

Buffett has figured out these fundamentals not only from his mentor Benjamin Graham, but also by being a continuous learner and observing how the world, the markets and investor psychology works.

Let’s dive deeper into each of these principles to understand what he figured out and implemented in his investing approach.

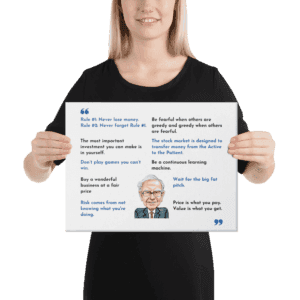

Rule #1 – Don’t Lose Money

What’s the distilled idea: Don’t lose money, and have a high bar for what companies you choose to invest in, so that you don’t lose money. Buffett often uses the analogy of using a punch card while investing in a stock, where this punch card only has 20 holes, i.e.you can only buy 20 stocks over a lifetime. This sets a high threshold for what to buy. The overarching rule of not losing money is supported by philosophies such as ‘margin of safety’ and ‘big fat pitch’ which we will discuss below.

Why’s it important: In investing, protecting the downside is significantly more important than taking big, bold bets. While shooting for the moon and ‘high risk equals high reward’ is the conventional thinking, Buffett looks for low risk, high uncertainty situations where losing money is unlikely. Buffett also understood early on that not losing money was a necessary ingredient in the recipe of compounding

Example: Buffett applied the principle of inversion to avoid losing money. He studied how investors and businesses fail, and found that the reasons are usually around speculation, excessive leverage, bad management or uneconomic business models. Avoiding such situations meant that he avoided losing money.

Focus on the small, neglected area of the market

What’s the distilled idea: Focus on the small, micro cap companies which are neglected by the bigger players in the market, that’s where the inefficiencies and hence the big opportunities are found.

Why’s it important? Institutional investors and fund managers usually go after the mega caps or large companies, hence these stocks are overcrowded, making it difficult to find bargains. The smaller end of the market is lucrative, because it’s under-followed and has the potential of finding opportunities that are hiding in plain sight.

Example: When Buffett ran his partnership between 1957-1968, most of his bets were in small, unknown stocks such as Dempster Mills. He purchased Dempster well below the liquidation value which meant he was able to generate handsome returns. Buffett has said that if he had to start investing from scratch again, the small end of the market is where he would focus on.

Stocks are fractional ownership stakes in the business

What’s the distilled idea: Stocks are not just pieces of papers or ticker symbols on an app. They are fractional ownership stakes in a business. When you hold a stock, you are a part owner of a business. Buffett learnt this key concept from Ben Graham,

Why’s it important? It changes your perspective because you switch into the mentality of looking at businesses as a whole. Instead of buying Nvidia for $140 a share, you think about buying the whole company by paying the current market capitalisation I.e. $3.4 trillion. Is it worth more, or is it worth less than that? It forces you to think about the business that’s under the hood of the ticker symbol.

Thinking of yourself as a part-owner of a business also means you are less tempted to sell just because the market values the business 10% higher than the previous year. Example: Buffett held on to stocks like Coca Cola, American Express for decades, because he saw himself as a silent partner in these highly cash generative businesses.

Price is what you pay, value is what you get

What’s the distilled idea – Each business has a stock price, and also an intrinsic value (defined as the present value of future cash flows from the business). Investors must understand the difference between price and value and they must buy stocks that are trading well below the intrinsic value of the underlying business.

Why’s it important – most people don’t put in the effort to calculate the intrinsic value of the business. Knowing the value of a business is empowering, as it allows you to identify situations where there’s a significant dislocation between price and the value. Buying stocks that are significantly undervalued is how Buffett made his fortune.

Example: When Buffett bought See’s Candies for $25 million in 1972, he paid a multiple of around 14 times earnings which is a high multiple for private deals. However, Buffett knew that See’s could generate a lot more cash as See’s was an established brand that had pricing power and opportunities to expand its operations. See’s earned more than $80 million in 2023, and has paid billions of dollars to Berkshire over the decades.

If you are the net buyer of Stocks, you should hope that stock prices go down, not up

What’s the distilled idea: Buffett explained this mindset in one of his lectures. He asked this question (paraphrased)- “if you are a regular buyer of burgers, would you want burgers to be cheaper or more expensive over time? (The answer is cheaper, obviously). Similarly, if you are a regular buyer of stocks (like most young people are) you want stocks to be cheaper.

Why’s it important? This is an unconventional idea, because most investors don’t think like that. They want stocks to go up immediately after they buy it. But Buffett’s point is – if you buy a great business below its intrinsic value, and the stock price drops substantially, it means that the stock is a better bargain than before. It is an opportunity to buy more, if your original thesis still holds true.

Example: Buffett has done this multiple times, buying more of the stocks he already owns, when they dipped significantly below his estimated intrinsic value. He bought billions of dollars worth of stocks in the 2008 financial crisis as well as the 2020 COVID stock market crash, when stocks were, in his words, ‘for sale’. This idea changed my thinking about stocks and stock prices. As Buffett has often said, you shouldn’t let the stock prices guide/influence you.

A caveat to this idea is that it’s important to understand why the stock is selling off and whether it changes your original thesis. If it does, then the drop in stock price may be a cause of concern.

Stay within your circle of competence

What’s the distilled idea? Investing is hard in itself. Buffett cultivated the habit of only investing in businesses that he understood well. And the ones that he didn’t, he simply put them in the ‘too hard ‘ basket.

Why’s it important? Not knowing the business deeply can be a disadvantage for an investor. Hence investors should let these go since there are “no called strikes” in investing, as Buffett says. It also helps you to narrow down the universe of thousands of listed businesses.

Example: Despite being close friends with Bill Gates, Buffett never invested in Microsoft because he said it wasn’t a domain he understood well. He was not able to predict whether Microsoft will still be in business 100 years in the future. But he could predict Coca-Cola would. Buffett exercised discipline in staying only within his circle of competence.

Invest with a margin of safety

What’s the distilled idea: Buffett once said that he wasn’t interested in buying a stock for $80 if the intrinsic value was $83. He looked for opportunities where the upside was significantly higher. For e.g. when he purchased shares in the Washington Post, the business was valued by the market at $80 million, whereas Buffett’s estimate of the value of that business was around $400 million.

Why’s it important? Having a Margin of safety while buying stocks (i.e. buying stocks which are significantly undervalued) helps you to protect against losses (Rule #1 of investing). Keeping a Margin of safety also acts as a protection against unexpected events in the market or within the business.

Example: When Buffett bought Berkshire Hathaway in 1965, then a textile mill, his purchase price was well below the liquidation value of the business. He bought the entire business because he knew that in the worst case scenario, he could just liquidate it and extract more value than what he paid for.

Wait for the big fat pitch

What’s the distilled idea: Buffett says that the clear-cut opportunities are rare in investing, so you must patiently wait for them. And when you find them, you have to make the most of them by swinging big. The fat pitch opportunities arise if a stock is significantly undervalued.

What do you do when you get a big fat pitch? You swing big, i.e bet a sizable portion of your portfolio on such opportunities. While this goes against the conventional investing principle of ‘diversification’ (most professional investors manage a basket of 20-50 stocks), Buffett believes that “there is no point in putting money on your 40th best opportunity.” Hence when he saw fat pitches, he put in huge sums of money, such that at times his one stock made up more than 25% of his portfolio.

Why’s it important? Betting big on rare opportunities led to Buffett and Munger earning outsized returns. Buffett averaged a staggering ~30% return per annum during the decade of managing the Buffett partnerships in the 1960s where he often held ~8 to 10 stocks. He wouldn’t have achieved the same returns if he had put restrictions around position sizing in his partnership (i.e. held 50 stocks).

Example: When Buffett and Partners purchased a controlling stake in Dempster Mills at a large price to it’s book value, he bet 20% of the partnership’s portfolio on this stock.

Warren Buffett Figurine – Limited Edition

Warren Buffett Figurine – add a touch of timeless wisdom to your space with unique collectible. Crafted with cutting-edge full-color 3D printing technology, this vibrant figurine is durable, high-quality, and shipped in a premium magnetic gift box. Perfect for your library, study, or as a unique gift for fans of the Oracle of Omaha.

Volatility can be your friend

What’s the distilled idea: Volatility in the stock market can be tremendously advantageous for long term investors, as short term corrections in the stock price can present huge opportunities if the investment thesis is bullish in the long term.

Why’s it important? Investors are a fickle bunch, and often operate in herds. Hence a short term sell-off in a stock could be an exaggerated market reaction. Investors who can spot these anomalies can make big returns.

Example: the American Express stock sold off significantly due to the Salad oil scandal in 1963. This was a fraud perpetrated by a borrower who gave falsified documents to American Express to borrow money. The size of the fraud was around $175 million, which was a substantial amount for American Express at the time. The stock price dropped by 50% when the news of the scandal broke.

Buffett found that the fundamentals of the business were strong, Although AmEx had a well-known banking division, the majority of its profits came from its Traveler’s Cheque and Credit Card divisions, which were growth businesses.

As Buffett expected, American Express survived this situation and between 1964 to 1973 the stock returned a phenomenal 1,000% (i.e. CAGR of 58%).

Long term orientation is a huge advantage for retail investors

What’s the distilled idea: The average holding period for investors today is less than 6 months, hence buying a stock with the intention of holding it for 10 years can make a significant difference in stock selection as well as in investment returns. Buffett says this is a huge advantage for retail investors.

Why’s it important? As Charlie Munger once said, “the big money is not in the buying and the selling, in the waiting”. Compounding returns takes time, hence once you have bought a great business, it’s important to hold it for the long term so that the business can generate returns for its shareholders.

Example: Buffett’s investment in Apple Inc was a master stroke which has earned Berkshire Hathaway a sweet 27% average annual return over 8 years.

These 10 philosophies are powerful, timeless wisdom that Buffett figured out and implemented relentlessly in his lifetime. Remarkably, he’s shared these openly, freely and repeatedly. Its important to understand, remember and use these big ideas in our investing journey!

Shop Warren Buffett Collectibles

‘Notebook of Wisdom’ with 160 Investing Quotes

Original price was: $99.00.$69.00Current price is: $69.00.Canvas Print with Warren Buffett success quotes and caricature

Original price was: $119.00.$89.00Current price is: $89.00.

Circle of Competence Coffee Mug with Warren Buffett Quotes

Price range: $36.99 through $42.99

Continue Reading

A Beginner’s Guide to Value Investing in the Stock Market

Stay Hungry, Stay Foolish: Transformative Lessons from Steve Jobs

Volatility Is Opportunity

Investing Principles for Aspiring Investors

Peter Lynch’s Investing Philosophy